Talking to Your Bank About Foreclosure in Hampton Roads VA

By Virginia Cash Real Estate ·

Facing foreclosure in Hampton Roads? Read our full avoid foreclosure guide — sell before the auction for your timeline and options.

How to Talk to Your Bank About Foreclosure in Hampton Roads — And Why Time Is Everything

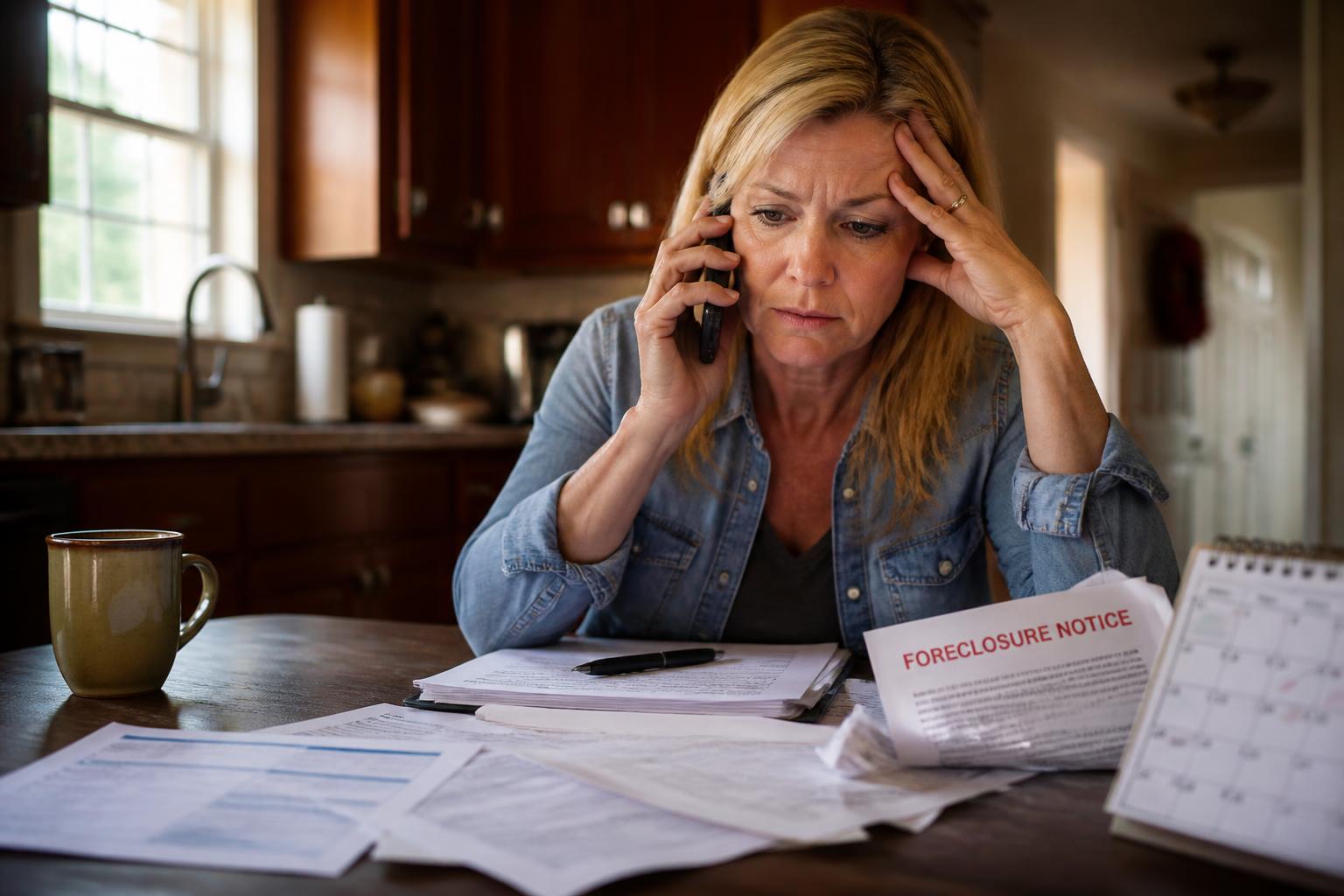

If you've fallen behind on your mortgage in Virginia Beach, Norfolk, Chesapeake, Hampton, Newport News, Portsmouth, or Suffolk, the most important call you can make is the one to your lender. Banks aren't villains in this story — but they are businesses on a clock, and the closer you get to your foreclosure auction date, the less they're willing or even able to talk to you.

Virginia Cash Real Estate has worked alongside Hampton Roads homeowners facing foreclosure since 2015, and the single biggest mistake we see is silence. Homeowners avoid the bank because the situation feels embarrassing or hopeless — and by the time they're ready to talk, the window has closed.

Why Calling Your Bank Early Matters

Mortgage lenders have entire departments — usually called Loss Mitigation or Homeowner Assistance — built specifically to help borrowers avoid foreclosure. These teams can offer:

- Forbearance — a temporary pause or reduction in payments

- Loan modification — a permanent change to your loan terms (rate, length, or balance)

- Repayment plans — a structured way to catch up missed payments over time

- Short sale approval — permission to sell the home for less than what's owed

- Deed in lieu of foreclosure — handing the property back without going through auction

All of these options exist. None of them happen automatically. You have to call and ask — and you have to do it early.

The 30-Day Rule: Once the Auction Is Set, Banks Aren't Required to Talk to You

This is the part most Hampton Roads homeowners don't know until it's too late: once you are within 30 days of your scheduled foreclosure auction date, your lender is no longer legally required to engage in loss mitigation discussions with you.

Federal mortgage servicing rules (the protections under Regulation X of RESPA) require servicers to evaluate a complete loss mitigation application only if it's submitted more than 37 days before a scheduled foreclosure sale. Inside that 30-day window, the bank can — and often will — refuse to review modification requests, decline forbearance discussions, and simply proceed to auction.

That doesn't mean the bank can't talk to you. It means they don't have to. And in our experience, most won't. By that point the foreclosure attorney is in control of the file, the trustee's sale is advertised in the newspaper, and the bank's incentive is to let the process finish.

The practical takeaway: if your auction date is set, you have a hard countdown. Every day you wait to act is a day closer to losing both your home and any equity you have in it.

How to Actually Talk to Your Bank — A Step-by-Step Approach

When you call, you're not begging for mercy — you're a borrower exercising rights the federal government created specifically for this situation. Approach the call like a business conversation.

Step 1 — Call the number on your mortgage statement and ask for Loss Mitigation Don't talk to general customer service about a missed payment. Ask specifically for the Loss Mitigation or Homeowner Assistance department. Write down the name and direct extension of every person you speak with.

Step 2 — Be honest about your situation Lenders have heard every story. They want to know what changed — job loss, medical bills, divorce, military relocation, death in the family — and whether the hardship is temporary or permanent. Honesty gets you reviewed; vagueness gets you ignored.

Step 3 — Request a loss mitigation application in writing This is the formal package that starts the clock on the bank's legal obligation to evaluate your situation. Submit it complete, with every document they ask for. An incomplete application doesn't trigger the protections.

Step 4 — Document everything Keep a notebook. Date, time, name, what was said, what was promised. If a bank later claims you never asked for help, your notes are your defense.

Step 5 — Don't stop because they say no the first time A denial of one option (say, modification) doesn't mean every option is off the table. Ask what else is available. Ask for a supervisor. Ask for the loss mitigation specialist assigned to your file.

Ready to Sell Your Hampton Roads Home Fast?

Virginia Cash Real Estate buys houses across Hampton Roads for cash — no repairs, no fees, no commissions. Get a fair cash offer within 24 hours.

What If You've Already Missed the Window?

If your Hampton Roads property is within 30 days of auction and the bank has gone quiet, you still have options — but they get narrower fast.

Sell before the auction. A cash sale that closes before the trustee's sale date stops foreclosure cold. The mortgage gets paid off at closing, the foreclosure is cancelled, and any equity above what you owe goes to you instead of being wiped out at auction.

This is exactly what we do at Virginia Cash Real Estate. When a homeowner calls us with a foreclosure auction date weeks or even days away, we move on their timeline. We've closed deals in as little as seven days to beat a trustee's sale — and we've helped families across Hampton Roads walk away with cash in hand instead of a foreclosure on their credit.

File for bankruptcy. Chapter 13 in particular can halt a foreclosure auction through an automatic stay. This is a serious legal step that should be discussed with a Virginia bankruptcy attorney — but it's a real option in the final hours.

Negotiate a postponement. Occasionally a lender will postpone a sale if you have a signed purchase contract in hand. This is one of the strongest reasons to involve a cash buyer early — a contract is leverage.

Why Hampton Roads Homeowners Wait Too Long (And How to Stop)

The pattern is heartbreakingly consistent. A homeowner falls behind. They open the first late notice, then stop opening the mail. The certified letters pile up. The phone calls go to voicemail. Months pass. By the time they're ready to face it, the auction date is two weeks out and the bank won't return calls.

If that's you — call us today, not tomorrow. Even if you don't end up selling to us, we'll tell you honestly whether you still have time to work directly with your lender, whether a short sale is realistic, or whether a fast cash sale is your best path to walking away whole.

Frequently Asked Questions

How many missed payments before the bank starts foreclosure in Virginia?

Most lenders begin formal foreclosure proceedings after 90 to 120 days of missed payments. Virginia is a non-judicial foreclosure state, which means once started, the process can move from notice of sale to auction in as little as 14 days.

Can the bank really refuse to talk to me once the auction is scheduled?

Yes. Federal servicing rules only require lenders to evaluate complete loss mitigation applications submitted more than 37 days before a foreclosure sale. Inside that 30-day window the bank can decline to engage entirely.

Will calling the bank put me into foreclosure faster?

No. Missing payments triggers foreclosure — not the call. Calling early almost always slows or stops the process; staying silent guarantees it continues.

Can a cash sale really stop a foreclosure auction in Hampton Roads?

Yes — as long as closing happens before the trustee's sale date. We've helped families across Virginia Beach, Norfolk, Chesapeake, Hampton, Newport News, Portsmouth, and Suffolk close in seven to fourteen days specifically to beat an auction.

What if I have equity in the house?

A foreclosure auction often wipes out homeowner equity — the property sells for what's owed, not what it's worth. A cash sale before auction lets you capture that equity instead of losing it.

Talk to Someone Who Understands Hampton Roads Foreclosure Timelines

Virginia Cash Real Estate has been helping homeowners across Hampton Roads stop foreclosure since 2015. We've closed on 100% of the properties we've put under contract, and we move on your timeline — not ours. If you're behind on payments, facing an auction date, or just want to understand your options, call Matt or Ben directly at [(757) 699-4796](tel:7576994796) or fill out our online form for a response within one business day.

The earlier you call — the bank or us — the more options you have.